MENA startups raise $1.7 billion in H1 2026 despite regional uncertainty

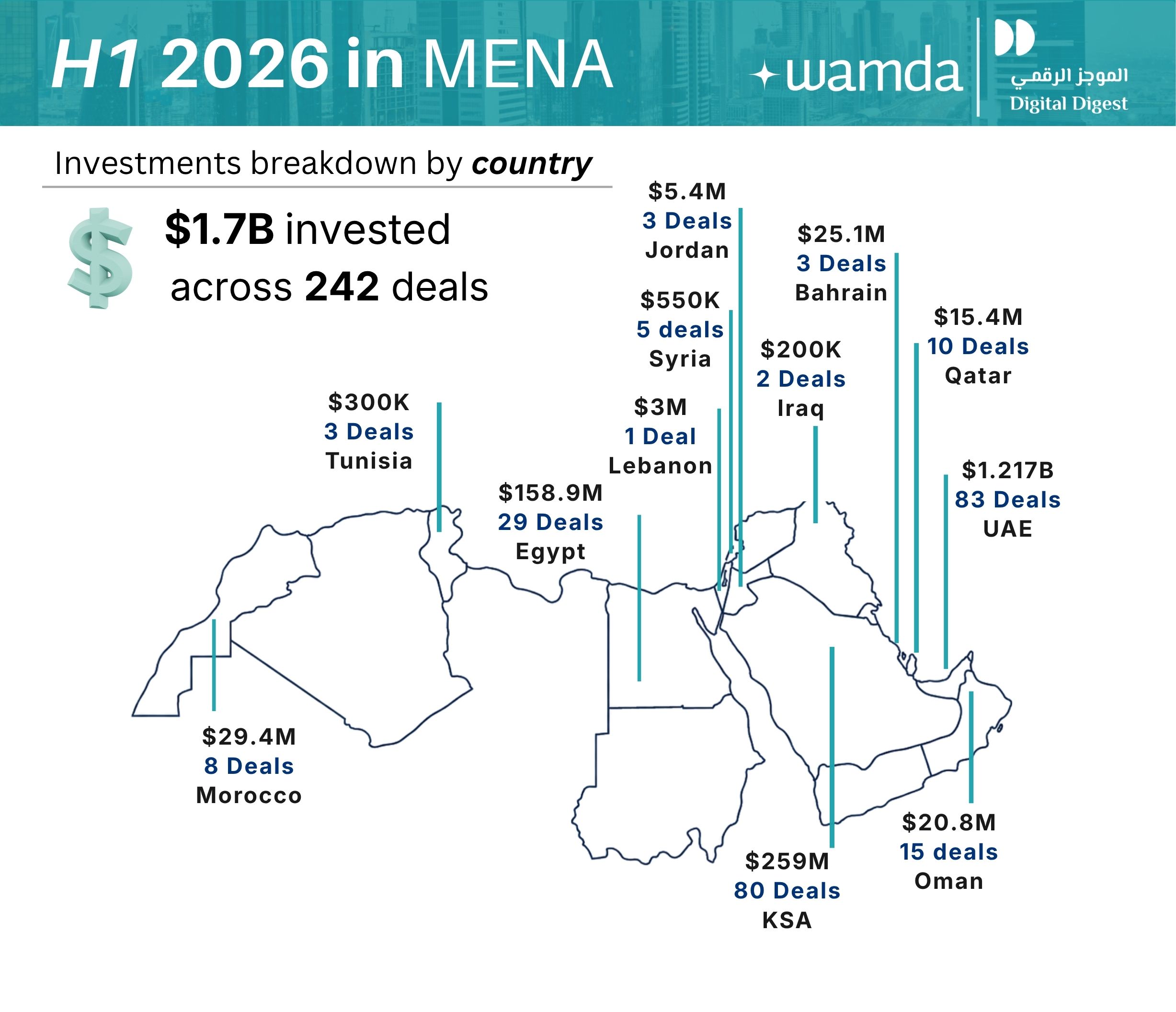

The Middle East and North Africa's startup ecosystem attracted $1.7 billion across 242 funding rounds during the first half of 2026, as investors continued deploying capital despite one of the region's most volatile geopolitical periods in recent years. While total funding declined 18% from the $2.1 billion raised in H1 2025, the underlying composition of capital suggests a more measured market rather than one in retreat.

Deal volume fell more sharply, down 28% year on year, reflecting greater investor selectivity and fewer transactions. At the same time, the market became less dependent on debt financing. Debt accounted for 29% of total capital raised during H1 2026, compared with 44% a year earlier, indicating that equity investment represented a larger share of overall funding.

Rather than signalling a broad contraction, the first half of the year reflected a market recalibrating amid heightened regional uncertainty, with capital increasingly concentrated around larger ecosystems, established sectors and companies with clearer paths to scale.

Q2: Capital becomes more selective

The second quarter mirrored the broader trends seen across the first half. MENA startups raised $793.5 million across 104 deals, down 16% from the first quarter, while transaction volume declined 25%.

The UAE remained the region's investment engine, attracting $591 million across 37 deals, followed by Saudi Arabia with $102 million through 23 transactions, while Egypt ranked third with $72.6 million across 17 deals.

Logistics emerged as the quarter's largest sector by capital deployed, raising $300 million through only two transactions, highlighting investors' willingness to back fewer but substantially larger deals. Fintech followed with $278.6 million across 26 deals, maintaining its position as the region's most active sector by transaction count, while Enterprise AI ranked third after raising $67 million through two deals.

Funding remained heavily skewed towards younger companies. Early-stage startups secured $211 million across 63 rounds, accounting for the overwhelming majority of transactions despite representing only around a quarter of total capital deployed. Later-stage activity remained limited, with just four rounds worth $111.4 million, while 30 companies chose not to disclose their funding stage.

Fintech continues to dominate as capital concentrates

Fintech extended its lead as MENA's largest investment destination during the first half, attracting $708 million across 51 rounds, comfortably outpacing every other vertical.

Logistics ranked second with $315 million, largely driven by a handful of sizeable transactions, while proptech climbed into third place after securing $241 million across 18 deals.

Stage distribution paints a similar picture. Early-stage startups accounted for the overwhelming majority of fundraising activity, with 172 companies raising a combined $444 million. At the other end of the spectrum, only 11 later-stage companies secured funding, attracting $224 million.

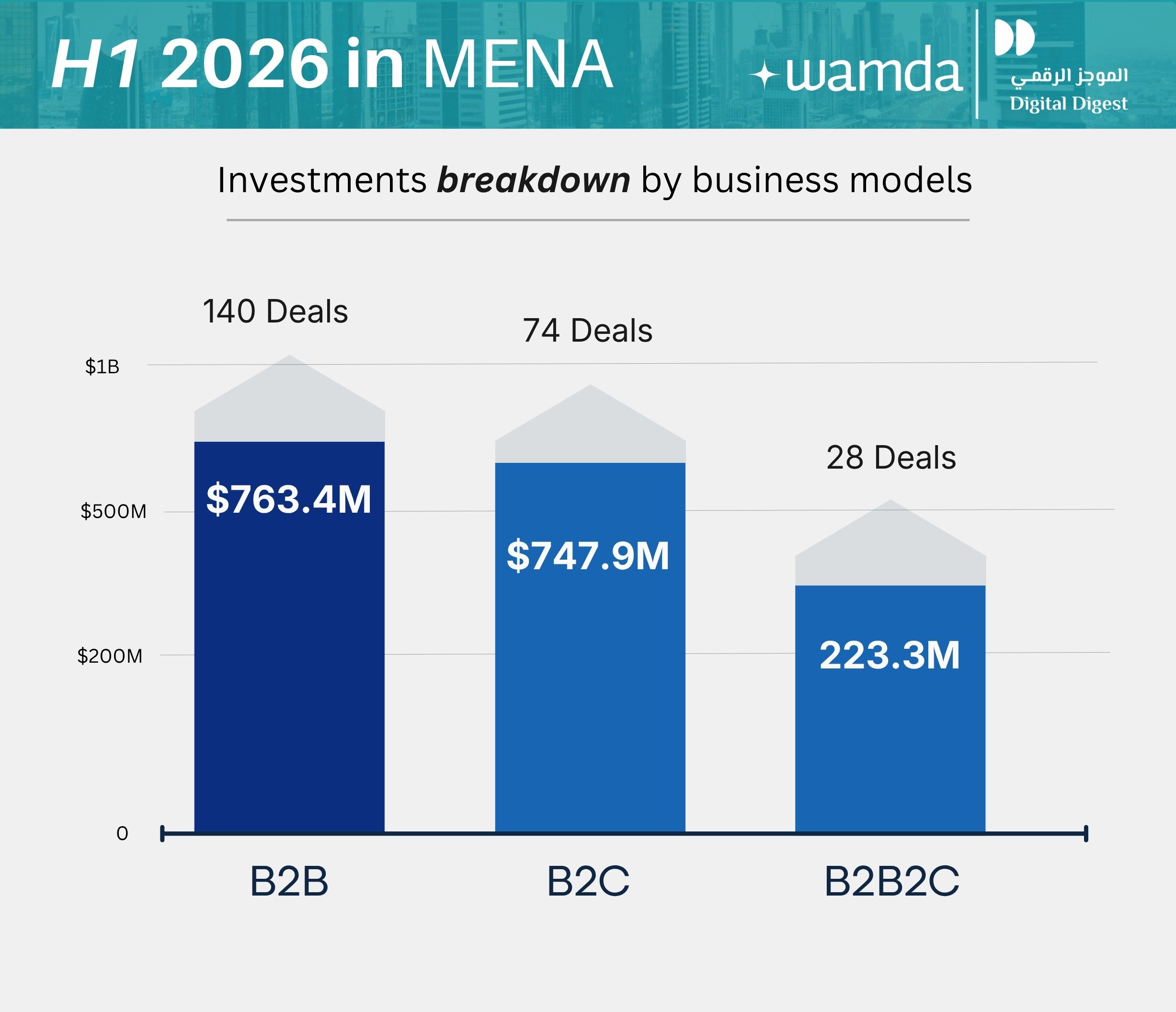

Business model preferences also remained largely unchanged. B2B startups continued to receive the largest share of investor attention, raising $763.5 million across 140 deals, narrowly ahead of B2C companies, which secured $748 million. Hybrid business models accounted for the remaining investment.

The funding gap for female founders widens further

Gender diversity remained one of the ecosystem's weakest indicators.

Male-founded startups captured approximately 95% of all capital deployed during H1, raising $1.6 billion across 213 deals. Female-founded companies secured just $2.5 million through 14 transactions, representing only 0.14% of total funding, while mixed-gender founding teams accounted for the remainder.

The figures underline that, despite continued ecosystem development, access to venture capital remains overwhelmingly concentrated among male founders.

UAE extends its regional lead

The UAE further consolidated its position as MENA's dominant startup market during the first half of 2026.

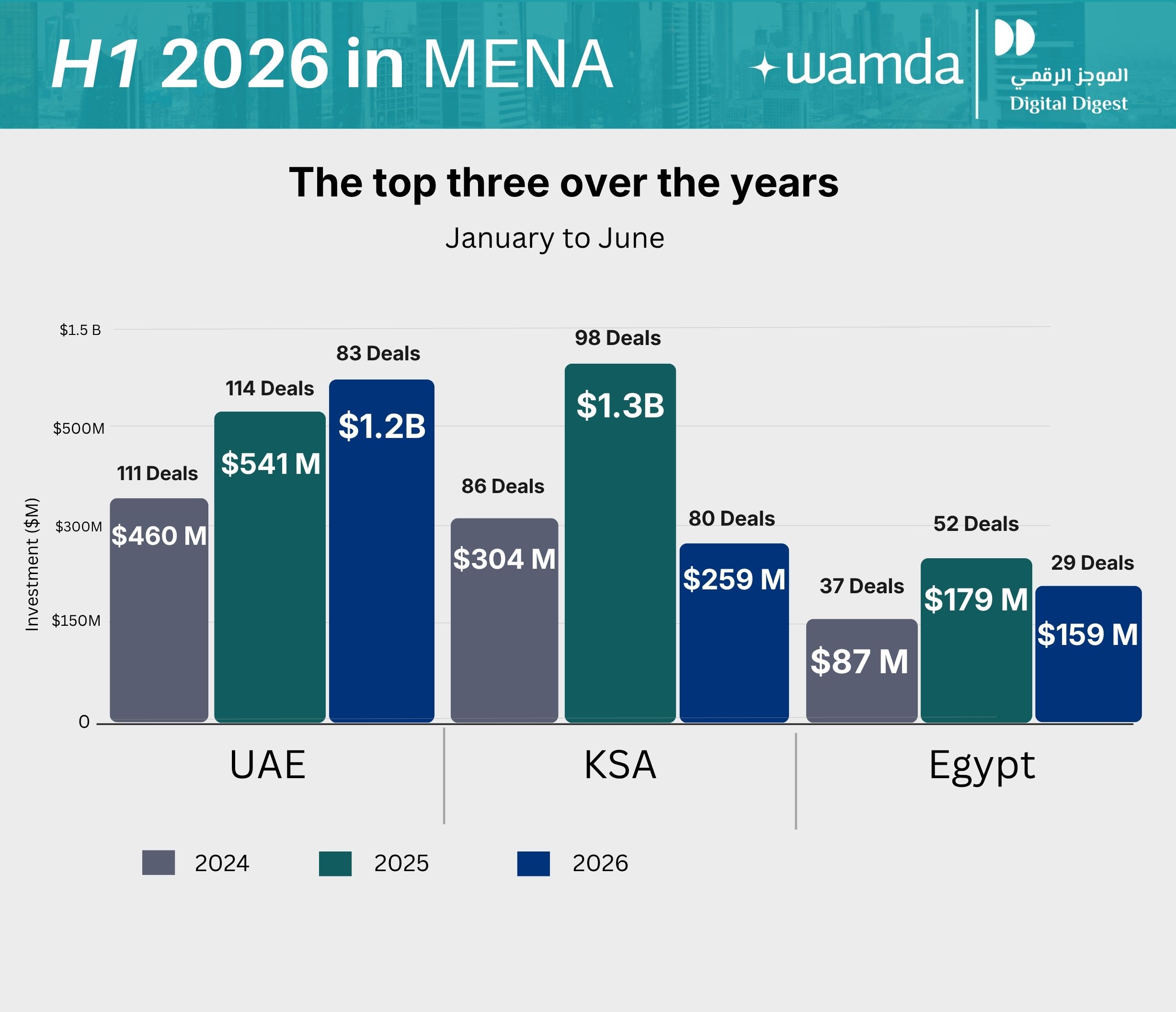

Startups based in the country raised $1.2 billion across 83 deals, accounting for roughly 70% of all capital invested across the region and marking a remarkable 125% increase compared with H1 2025.

Fintech remained the country's largest vertical, attracting $409 million across 20 deals, equivalent to roughly one-third of all UAE funding. Logistics followed after securing $300 million through two transactions, while proptech ranked third with $215 million across 13 deals.

The maturity of the UAE ecosystem also became evident in its later-stage activity. Eight of the region's later-stage rounds took place in the UAE, reinforcing its role as the primary destination for scale-stage companies. Debt financing represented 35% of capital raised through six transactions, while early-stage startups attracted 11% of total funding. Fifteen companies did not disclose their funding stage.

Saudi Arabia slows after a record year

Following an exceptional 2025, Saudi Arabia recorded a more measured first half in 2026, raising $259 million across 80 deals, an 81% decline in capital compared with the same period last year.

Fintech continued to dominate the Kingdom's funding landscape, accounting for $176 million, or 68% of total investment, across 13 startups. E-services ranked second with $15.2 million, followed by healthtech, where five companies raised a combined $14 million.

Unlike the UAE, Saudi Arabia's market remained overwhelmingly early stage. Startups at the earliest stages secured $201 million across 69 rounds, while no later-stage transactions were recorded during the period. Debt financing accounted for only 11% of total capital.

The sharp year-on-year decline should also be viewed in the context of an unusually strong comparison base. Saudi Arabia led regional fundraising throughout 2025, supported by several exceptionally large transactions. While geopolitical tensions and broader macroeconomic uncertainty likely weighed on investor activity during H1 2026, the Kingdom continues to benefit from one of the region's deepest founder pipelines, active institutional investors and an increasingly mature regulatory environment.

Egypt searches for fresh momentum

Egypt's startup ecosystem continued to operate in a challenging domestic economic environment, where access to venture capital remains constrained and larger funding rounds have become increasingly difficult to secure.

Startups in the country raised $158.9 million across 29 deals, representing an 11% decline from H1 2025.

Despite the softer headline figures, Egypt produced two later-stage rounds worth a combined $53 million, while debt financing contributed $22 million across two transactions. Early-stage companies attracted the remaining $57 million through 16 deals.

Fintech once again led investment activity, raising $82.3 million across seven transactions. E-commerce followed with $50.2 million through three deals, while logistics ranked third after securing $13 million across two rounds.

Looking ahead: Recovery remains uneven but the pipeline is intact

The first half of 2026 tested the resilience of MENA's startup ecosystem in ways few anticipated at the beginning of the year. While geopolitical tensions and broader economic uncertainty reshaped investment decisions, they did not bring capital deployment to a standstill. Investors became more selective, concentrating capital in mature ecosystems, proven sectors and companies with stronger fundamentals. If regional stability improves in the months ahead, the ecosystem enters the second half with an active funding pipeline, fresh venture capital ready to be deployed, and several high-profile IPOs and exits that could help reignite momentum across the market.

These monthly reports are a collaboration between Wamda and Digital Digest.