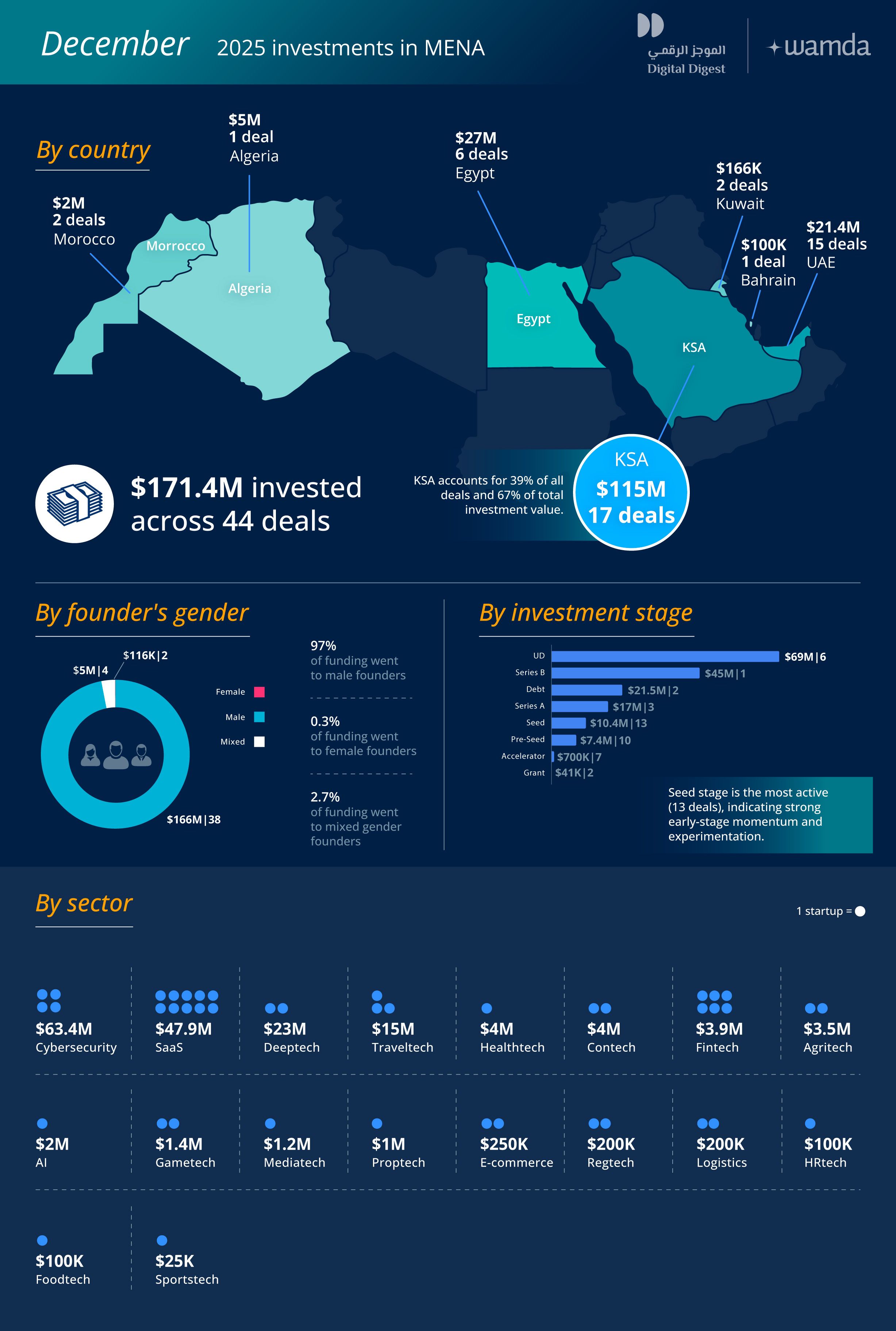

MENA startup funding ends 2025 at $171.5 million in December

Startup investment across the Middle East and North Africa (MENA) softened in December 2025, with 44 startups raising $171.5 million, marking a 38% year-on-year decline and a 24% drop compared to November. The pullback reflects a typical year-end slowdown, but the headline contraction masks a more nuanced shift in funding composition.

Stripping out debt financing from both months, December marginally outperformed November due to a reduced reliance on debt. In December, debt accounted for just 12.5% of total funding, signalling a return to more equity-led dealmaking towards the end of the year.

Saudi Arabia continues to dominate regional capital

Saudi Arabia once again emerged as the region’s most funded market, with 17 startups raising $115 million, accounting for 67% of capital deployed in December. Egypt followed at a distant second, with $27.3 million raised across six rounds, capping off a year marked by persistent funding pressure in the country.

The UAE ranked third, raising $21.4 million across 15 transactions, reflecting continued deal activity but smaller average ticket sizes.

Beyond the top three markets, Algeria, Morocco, Kuwait, and Bahrain collectively raised $7.5 million, highlighting the limited capital flowing to smaller ecosystems at year-end.

Fintech slips as cybersecurity leads sector funding

One of December’s clearest signals was the continued cooling of fintech. The sector fell outside the top five most funded verticals, ranking seventh, with just $3.9 million raised across six deals.

Cybersecurity led the month, attracting $63.4 million invested in four startups, followed by software-as-a-service (SaaS) companies, where 10 startups raised $47.9 million. Deeptech ranked third, securing $23 million across two transactions, reinforcing investor appetite for specialised, defensible technologies despite the broader slowdown.

Early-stage deals dominate activity, not capital

By deal count, December was clearly an early-stage month. Thirty-five early-stage startups raised $35.9 million, reflecting sustained investor engagement at the formation and validation stages. In contrast, three late-stage startups collectively raised $66.5 million, once again underscoring how a small number of large rounds continue to shape monthly funding totals. A further six startups did not disclose their funding stage.

B2B remains the preferred investment model

The business-to-business (B2B) model continued to dominate December’s investment landscape. B2B startups raised $154.7 million across 33 rounds, reinforcing investor preference for enterprise-led revenue models. Meanwhile, five consumer-facing startups raised $6.3 million, with the remainder flowing to six startups operating hybrid B2B and B2C models.

Gender funding gap remains pronounced

Funding disparities by gender persisted into the final month of the year. Female-founded startups raised just $116,000 across two deals, while mixed-gender founding teams secured $5 million via four rounds. The overwhelming majority of capital continued to flow to male-founded startups, closing 2025 with little indication of meaningful progress on gender inclusion in venture funding.

Looking ahead

December’s figures reinforce a defining theme for 2025: funding in MENA has become increasingly concentrated, selective, and unevenly distributed, with capital favouring a narrow set of markets, sectors, and business models. While monthly fluctuations offer useful signals, a full picture of how investor behaviour evolved over the year will only emerge at the aggregate level. Stay tuned for Wamda’s annual investment report, to be issued soon, where we break down 2025’s funding trends in depth, including capital flows by country, sector, stage, business model, and gender, alongside the structural shifts shaping startup investment across the region.